Early in my career at Ernst & Young, I learned something that has stayed with me through nearly three decades in finance: the story a company tells publicly and the story its numbers tell internally are rarely the same story. That gap, between the narrative and the math, is exactly where I spend most of my time as a fractional CFO and as the founder of Gazelle Ventures.

Nowhere is that gap more apparent right now than in SaaS. We’ve moved well past the era when a founder could flash a year-over-year growth chart and watch term sheets materialize. The market has sobered up, and the metric that increasingly separates companies worth backing from those burning daylight is one that balances two things most founders treat as opposites: growth and profitability.

That metric is the Rule of 40. And if you’re running a SaaS business at any stage, understanding it deeply is no longer optional.

So What Exactly Is the Rule of 40?

The Rule of 40 is straightforward in its arithmetic: add your annual revenue growth rate (as a percentage) to your profit margin (typically EBITDA margin), and the sum should be 40 or above. Simple enough. But what makes it powerful, and often misread, is what it actually permits.

A company growing at 60% annually can sustain a -20% EBITDA margin and still pass the test. A company that has matured to 15% growth needs to show 25% profitability to keep pace. The framework doesn’t demand profitability immediately, it demands that the combination of growth and margin reflects a business moving in a coherent direction.

Think of it as a health check for your entire business model. A company failing the Rule of 40 isn’t necessarily doomed, but it is telling you something important: you’re either growing too slowly for your burn, spending too aggressively for your growth, or both. That’s not a messaging problem, it’s a structural one.

Why Investors Have Re-Anchored Around This Number

For most of the last decade, venture capital flowed freely toward growth stories. If your ARR was compounding at triple digits, profitability was someone else’s problem, presumably future-you’s problem, post-exit. That logic made sense when cheap money was the backdrop and multiples were generous.

That backdrop has changed. Rates rose. Multiples compressed. IPO windows narrowed. And the investor community, from early-stage VCs to growth equity firms, began asking a different question: not “how fast are you growing?” but “how efficiently are you growing, and does this business have genuine staying power?”

The Rule of 40 answers that question in a single line. It’s become a shorthand for capital efficiency, and in today’s environment, capital efficiency is the story that closes rounds. When I’m preparing a SaaS founder for investor conversations, the Rule of 40 score is almost always the first metric we pressure-test together.

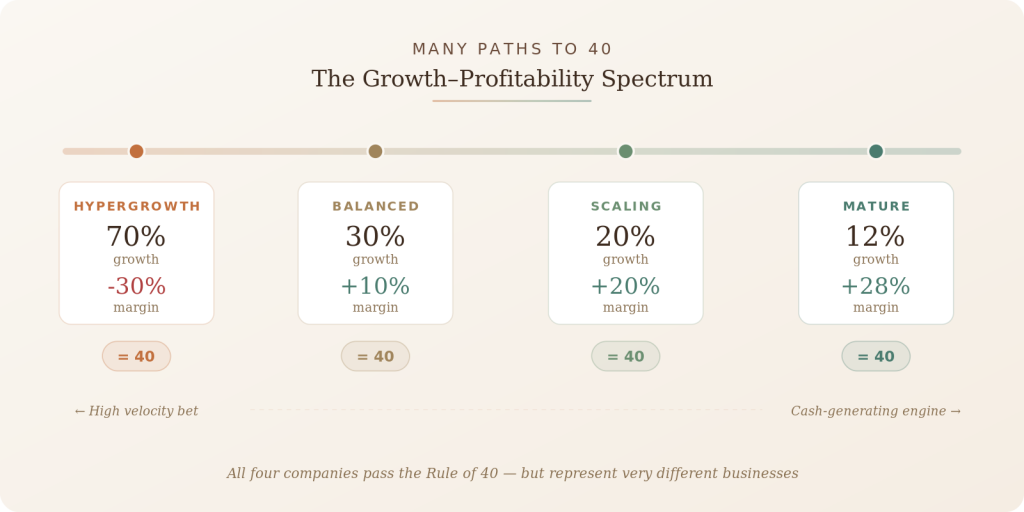

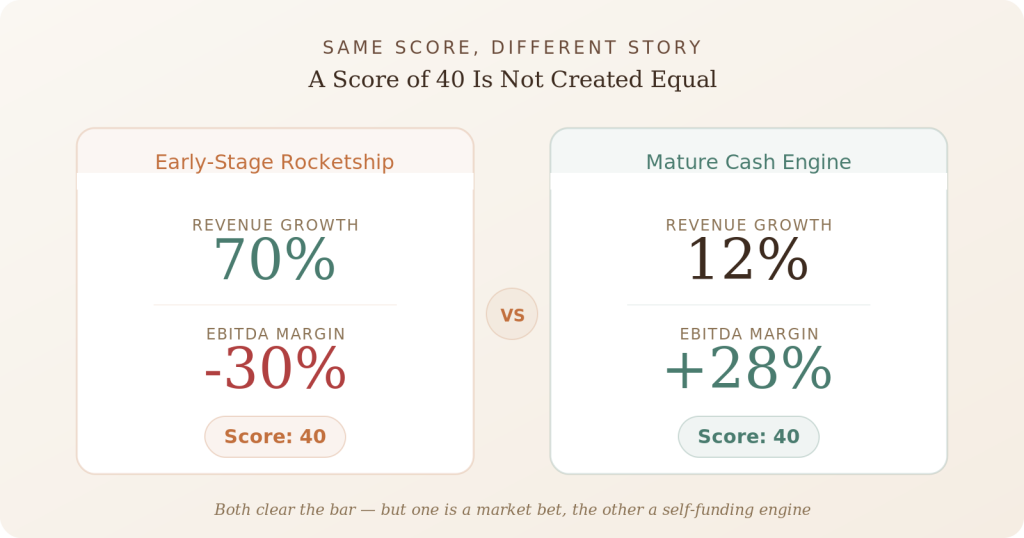

A Score of 40 Is Not Created Equa

Here’s the nuance that often gets lost: two companies can both score a 40 and be in very different situations.

A startup at 70% growth and -30% EBITDA is a fundamentally different investment than a mature SaaS business at 12% growth and 28% EBITDA. Both clear the bar. But one is a high-velocity bet on a large addressable market, and the other is a cash-generating engine that can fund itself. The Rule of 40 doesn’t tell you which is better, it tells you that both are operating within a defensible range.

The danger zone is when a company scores in the mid-to-high range on growth but is burning cash at a rate that isn’t matched by market traction. That’s the profile that often looks great from the outside and is actually fragile, and it’s precisely the situation I’ve seen catch founders off guard when markets tighten.

Sustainable growth, the kind that persists through funding cycles and market corrections, comes from building a business where efficiency and expansion reinforce each other, not where one paper-covers the other.

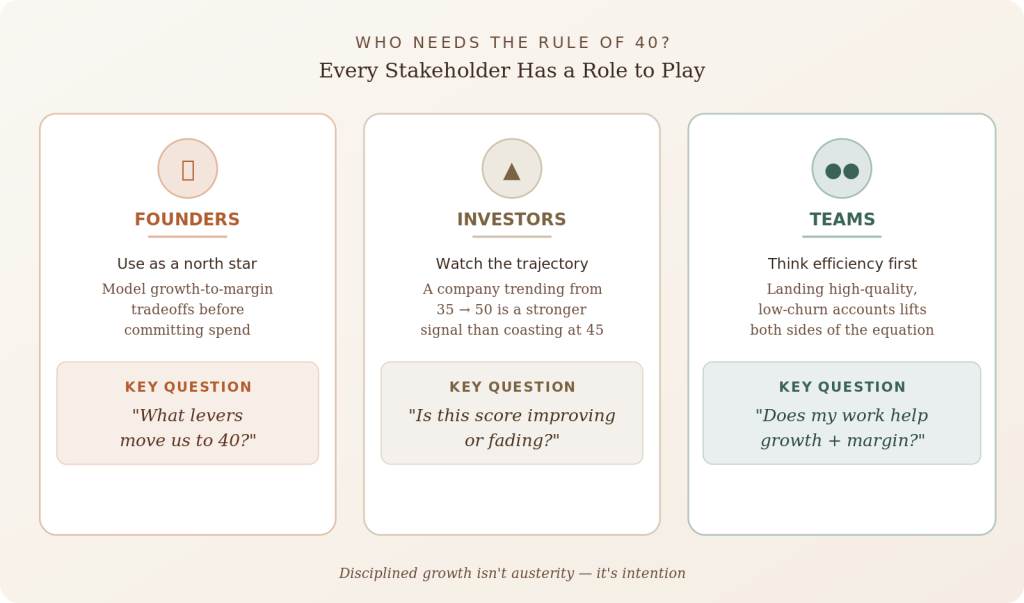

What This Means in Practice for Founders, Investors, and Teams

The Rule of 40 isn’t just a board meeting metric. It should shape how every stakeholder inside a SaaS business thinks and operates.

Founders need to treat the Rule of 40 as a north star, not a quarterly checkbox. This means modeling the relationship between growth investment and margin impact before committing to headcount plans, marketing spend, or new product initiatives. If you’re growing at 40% today and that growth requires a -25% EBITDA margin, you should be able to articulate exactly what levers you’ll pull to improve margin as growth normalizes, and when.

Investors, particularly those writing checks into early- and growth-stage SaaS, need to look at the trajectory, not just the current score. A company at 35 that is trending toward 50 is a better signal than one at 45 that is coasting. Due diligence on Rule of 40 companies should include understanding what’s driving the score and whether the underlying unit economics support it.

Teams, especially those who aren’t in finance, benefit from understanding this framework too. Disciplined growth isn’t about austerity; it’s about intention. When a sales team understands that landing high-quality, low-churn accounts improves both the growth and the profitability side of the equation.