One of the most common questions I get from founders is some version of: “Should I raise debt or equity?”The honest answer is: it depends, and more importantly, it depends on which kind of debt.

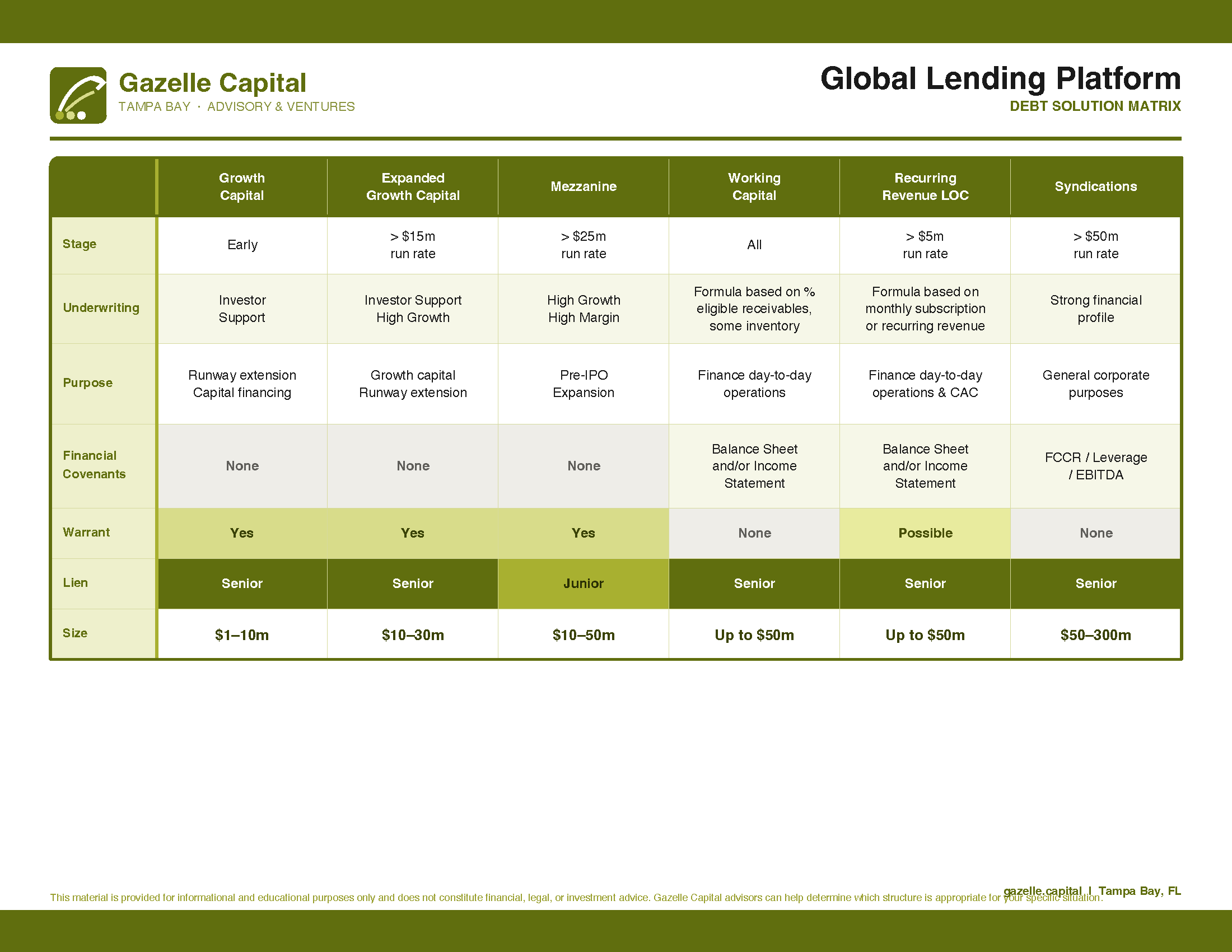

The matrix above maps six distinct lending structures used by growth-stage lenders. Each one is engineered for a different company profile, a different purpose, and a different risk appetite. Understanding the differences can save you significant dilution, preserve your covenant flexibility, and keep your balance sheet clean as you scale.

Here’s what I want founders to internalize:

Early-stage companies aren’t locked out of debt capital. Growth Capital and Expanded Growth Capital exist specifically for venture-backed businesses with investor support, no financial covenants required. The tradeoff is a warrant, which is far less costly than another equity round at a compressed valuation.

Working Capital and Recurring Revenue Lines are operational tools, not growth fuel. If you’re using them to fund CAC or bridge payroll, that’s fine — they’re designed for it. If you’re using them to fund product development, that’s a mismatch that creates risk.

Mezzanine debt is often misunderstood. It sits junior in the capital stack, which sounds scary, but for pre-IPO companies with high margins and $25m+ run rates, it’s frequently the most elegant pre-exit bridge available.

Syndications are a different conversation entirely. At $50m+ run rates with strong EBITDA, you’re no longer in venture debt territory, you’re in institutional lending, with covenants to match.

The right debt structure depends on your stage, your revenue quality, and what you’re actually trying to accomplish. If you’re evaluating options, this framework is a useful starting point: but the details matter enormously.

Gazelle Capital provides fractional CFO advisory services to growth-stage companies across the Tampa Bay region and beyond. Reach out if you’d like to talk through your capital structure.